As a founder, you are accountable for what you sign. That includes term sheets.

You cannot say “I didn’t know”. You cannot ask Visa or Amex for a chargeback. No excuses, no do-overs, no takesies-backsies.

This post will help you identify the key traps in a VC term sheet. Unlike our blog post on VC scams, these are all legal clauses that you just shouldn’t have signed on.

Let’s dig in.

(PS: Bookmark this post for later!)

Table of Contents

- Dirty clause 1: Full Ratchet Anti-Dilution ☠️☠️☠️☠️☠️

- Dirty clause 2: Participating Pref with No Cap ☠️☠️☠️☠️☠️

- Dirty clause 3: Multiple Liquidation Preferences ☠️☠️☠️☠️

- Dirty clause 4: Super Pro-Rata Rights ☠️☠️☠️

- Dirty clause 5: Founder Vesting Reset ☠️☠️☠️

- Dirty clause 6: Redemption Rights ☠️☠️☠️☠️

- Dirty clause 7: Full Board Control ☠️☠️☠️☠️☠️

- Dirty clause 8: Excessive Drag-Along Rights ☠️☠️☠️

- Dirty clause 9: Extensive Protective Provisions ☠️☠️☠️

- Dirty clause 10: Milestone-Based Tranches ☠️☠️☠️

- Dirty clause 11: Pre-Money Option Pool Increase ☠️☠️☠️

- Bonus: the dirty clause in the YC SAFE template!

- Conclusion: Watch out for your own greed

Dirty clause 1: Full Ratchet Anti-Dilution ☠️☠️☠️☠️☠️

This clause provides that if a future round happens at a lower price (=down round), the investors get their shares repriced entirely to that new lower price.

It’s dirty because it puts all the dilution on the founders, even if the down round is small or strategic.

For example, if the VC invested at $1.00/share and a later round happens at $0.50/share, their entire investment is repriced as if they had paid $0.50. This effectively doubles the VC ownership and dilutes you hard.

Instead, you should negotiate a fair downround.

Dirty clause 2: Participating Pref with No Cap ☠️☠️☠️☠️☠️

This clause states that investors get their investment back first (liquidation preference), then also share in remaining proceeds like common shareholders with no limit.

It’s dirty because it’s double-dipping. The investor gets too much. Even in a good exit, founders can get very little.

For example, let’s say the company exits for $30M. If the VC had invested $5M, they first take $5M, then also get, say, 25% of the remaining $25M, leaving the founders with far less than their equity suggests.

Dirty clause 3: Multiple Liquidation Preferences ☠️☠️☠️☠️

This clause stipulates that in the case of an exit, investors get 2x or 3x their money back before anyone else gets paid.

It’s dirty because in modest exits, the entire sale price could go to investors, leaving nothing for founders.

For example, if the VC invested $10M with a 3x liquidation preference and you sell for $25M, they take $30M. This is more than the total exit. You and your team get nothing.

Instead, an acceptable liquidation preference should be at 1x.

Dirty clause 4: Super Pro-Rata Rights ☠️☠️☠️

With this clause, an investor gets the right to buy more than their pro-rata share in future rounds to increase their ownership.

It’s dirty because it crowds out new investors, reduces founder leverage, and can lead to a power grab at the next round.

For example, if the VC takes 10% at seed but demands super pro-rata rights, they might take 30% at Series A, effectively locking in control for themselves.

They are the captain now.

Dirty clause 5: Founder Vesting Reset ☠️☠️☠️

This clause provides that founders have to re-vest shares they have already earned , typically on a 4-year schedule.

It’s dirty because you risk losing your own company if you leave or are pushed out early.

For example, raising a Series A with a 4 year vesting reset means that the founders would effectively own 0% of the company right after the raise – regardless of the many years of past work that came before the raise. The founders would slowly “regain shares” over the course of the next 4 years. This is understandable from the investors’ perspective: they want to lock in strategic people in the company. But it’s a huge sword hanging over the founders’ heads…

Dirty clause 6: Redemption Rights ☠️☠️☠️☠️

This clause states that investors can demand that the company repurchase their shares , usually after 3–5 years.

It’s dirty because it turns an equity investment into a quasi-loan to be repaid.

For example, if the VC invested $5M and activates redemption after 5 years, the company must repay the $5M, forcing a rushed sale or pushing the company to bankruptcy.

Dirty clause 7: Full Board Control ☠️☠️☠️☠️☠️

This clause stipulates that investors take control of the board by appointing a majority of directors.

It’s dirty because you lose decision-making power and can be overridden or even fired from your own company.

For example, if the VC installs 2 out of 3 board members, they can make all major decisions, including replacing you as CEO.

Remember: VCs aren’t your friends.

Dirty clause 8: Excessive Drag-Along Rights ☠️☠️☠️

With this clause, a small investor group can force the sale of the company and drag all shareholders along.

It’s dirty because you can be forced to sell even if you disagree, potentially at a bad price.

For example, if the VC owns 30% and gets a buyer at a lowball $20M valuation, they can force you to accept the deal even if you believe the company is worth more.

Dirty clause 9: Extensive Protective Provisions ☠️☠️☠️

This clause stipulates that minor operational decisions must be approved by the investor.

It’s dirty because it creates decision gridlock.

You want to hire a new team member? You want to change a feature? Tough luck, the VC doesn’t agree and you’re blocked.

That’s not entrepreneurship, that’s puppeteering.

Dirty clause 10: Milestone-Based Tranches ☠️☠️☠️

This clause states that the investment is split into tranches, released only after hitting specific milestones.

It’s dirty because you can be starved if you miss an arbitrary goal. Forecasts at early-stage are highly uncertain, and the founders are just bearing too much risk.

For example, if the VC commits $4M but only gives you $1M upfront and says the next $3M depends on hitting revenue targets, they can walk away if you fall slightly short.

Either they invest in the round, or they don’t.

Dirty clause 11: Pre-Money Option Pool Increase ☠️☠️☠️

With this clause, founders are required to expand the employee option pool BEFORE the investment , diluting their own shares.

It’s dirty because it lowers the effective valuation for founders. You give up more equity than you think.

For example, if the VC demands a 15% option pool increase pre-money, your stake gets diluted before their money even hits the cap table, effectively lowering your true valuation.

The right way to handle that would be (a) sizing the option pool based on a real hiring plan i..e don’t create a 15% pool if 7% is realistically enough, and (b) increase the option pool post-money.

Or if you really have to do it pre-money, bump up the valuation accordingly.

Bonus: the dirty clause in the YC SAFE template!

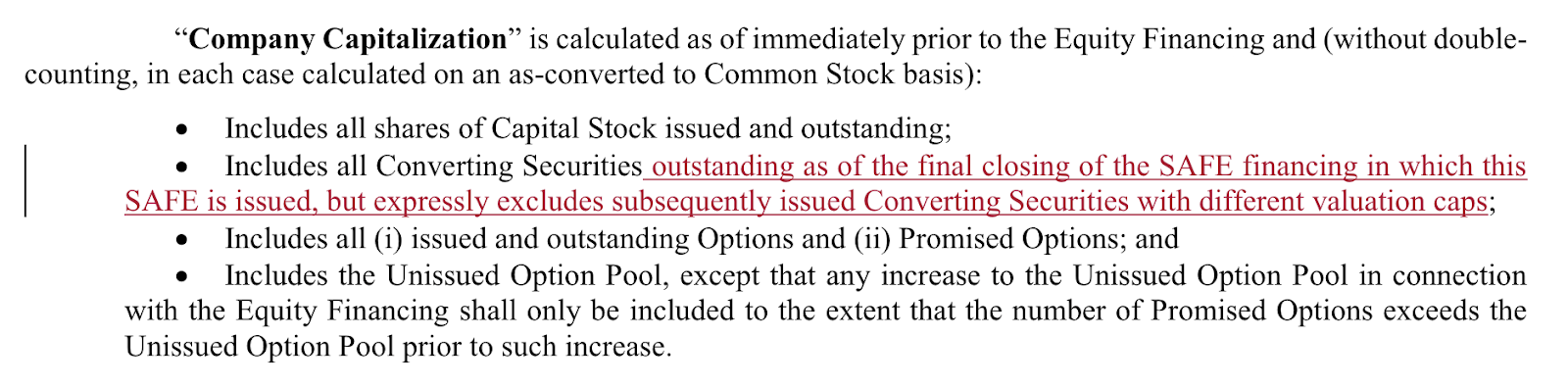

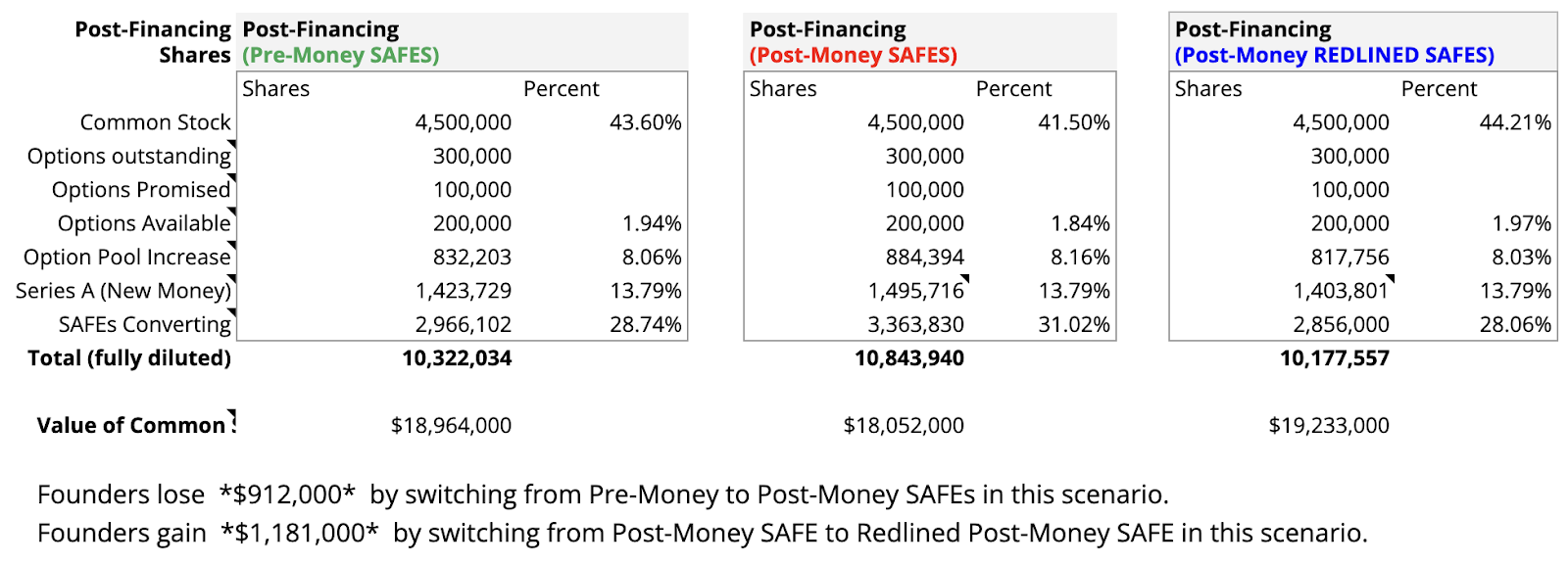

The YC post-money SAFE template (2018) is the most used fundraising instrument in the startup world.

Yet, it contains a clause you might call “dirty”.

This clause guarantees each SAFE investor a fixed ownership percentage that is protected from dilution by future convertible rounds.

It’s dirty because all the dilution from later SAFE or notes is pushed entirely onto the founders and employee pool, even if those rounds are at higher valuations. Over time, founders can lose significant equity without realizing it.

For example, if you raise multiple SAFE, each capped at 10% post-money, they don’t dilute each other, only you. By the time you reach a priced round, you may have unknowingly given up 40-50% of the company before any equity round has occurred.

Kudos to Silicon Hills Lawyer for pointing it out in their 2019 post “Why Startups shouldn’t use YC’s Post-Money SAFE” and publishing a redlined version of the YC SAFE template that fixes the issue (available here ).

They also built a free simulator in Google Sheets. Give it a try!

Conclusion: Watch out for your own greed

Why do founders fall for these dirty clauses?

- 20% of founders are ignorant. They just didn’t read that blog post.

- 40% of founders are desperate. They have to take a bad term sheet or go bust.

- 40% of founders, however, are victims of their own greed…

You see, when raising funds, some founders optimize for valuation over terms.

They want to say they “raised eight figures” or that the company “is worth $1B”. They trade dirty clauses for an ego boost. Big mistake.

When negotiating with VCs, valuation doesn’t matter as much as the terms.

So get informed. Put a good lawyer in your corner. And keep your greed in check.

Otherwise, you may end up the butt of a joke in HBO’s Silicon Valley.