By Tyler Durden,

In his final Global Economics Analyst report of 2021, Goldman's chief economist Jan Hatzius has published his favorite 10 charts to illustrate the key global themes that stood out this year and are likely to shape 2022.

In his brief previews, Hatzius writes that "the global economy recovered rapidly in 2021 as demand surged. Mass vaccinations and adaptation made growth less sensitive to infections although risk aversion to the virus remained high in Asia-Pacific for much of the year.Fiscal policy turned from a large boost in the spring into a modest drag in the US. However, policy remains more expansionary in the Euro Area."

Of course, 2021 was a year when Goldman's inflation forecasts - like those of most other career economists and Fed officials - were catastrophically wrong and the bank was forced to hike its year-end CPI and PCE forecast virtually every month as inflation went from "transitory" to not. That's why in his final note the chief economist writes that "following this very rapid rebound in demand, our short-run output gaps tightened into overheating territory in the UK and, to a lesser degree, in the EuroArea, and the US."

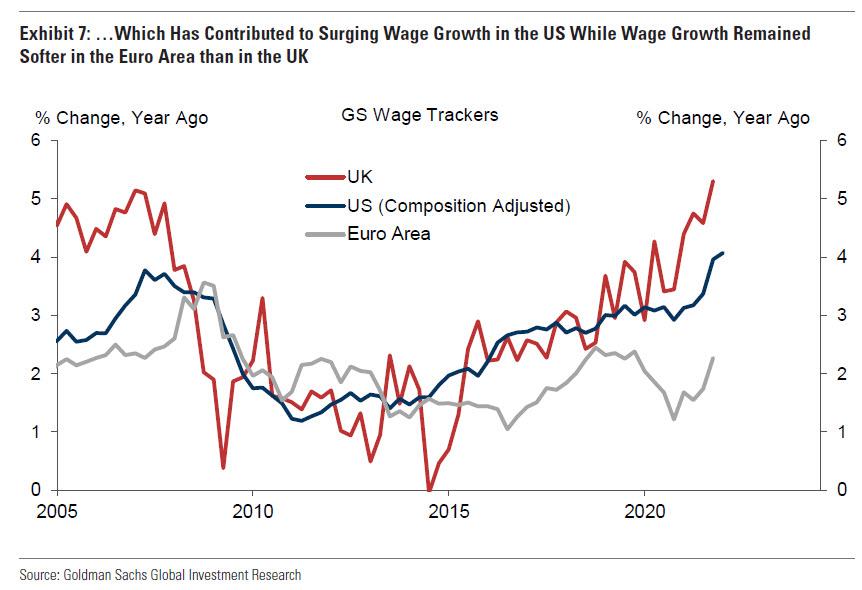

Not surprisingly, the Goldman economist admits that "the biggest surprise of the year was the global inflation surge, which was particularly pronounced for US goods, global energy, and Latin America." Meanwhile, persistent labor shortages boosted wage growth in the US and the UK,which remained softer in the Euro Area.

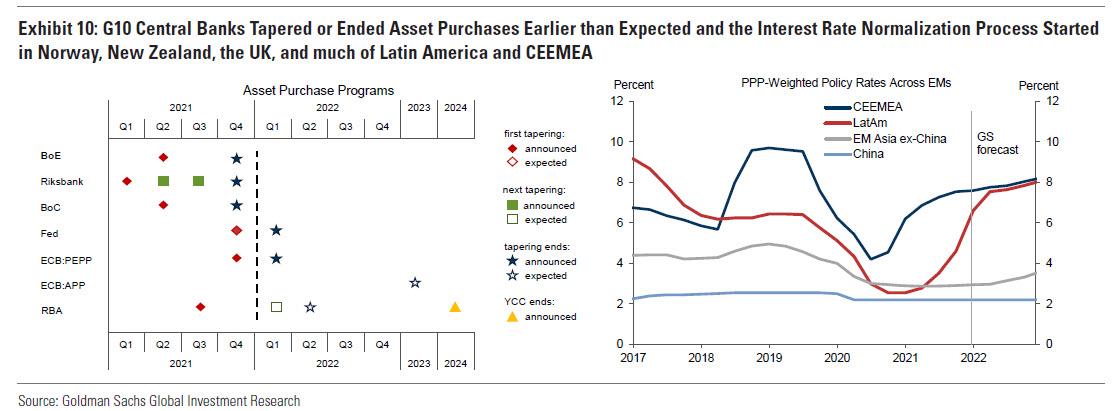

As a result, Hatzius concludes, "G10 central banks tapered or ended asset purchases earlier than expected. The interest rate normalization process started in Norway, New Zealand, the UK, and much of Latin America and CEEMEA, and is set to broaden and deepen in 2022."

So without further ado, here are Goldman's Top charts of 2021.

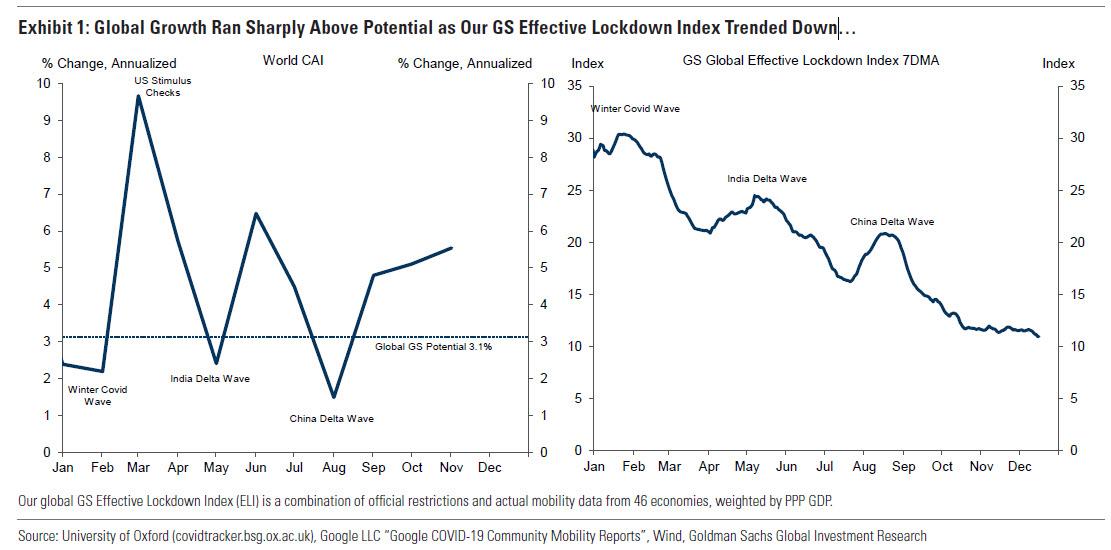

We start with global growth, which ran sharply above potential as the Goldman "Effective Lockdown Index" trended down.

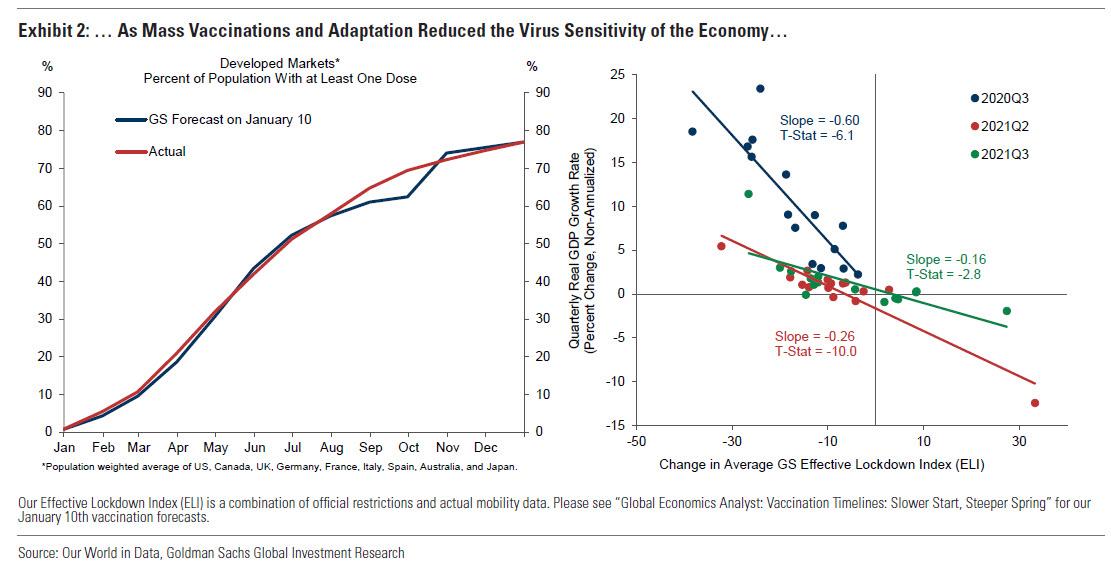

Unlike 2020, Goldman claims that mass vaccinations "reduced the virus sensitivity of the economy" although one should insert a big footnote here, as the Omicron variant appears to be prevalent almost exclusively among vaccinated individuals.

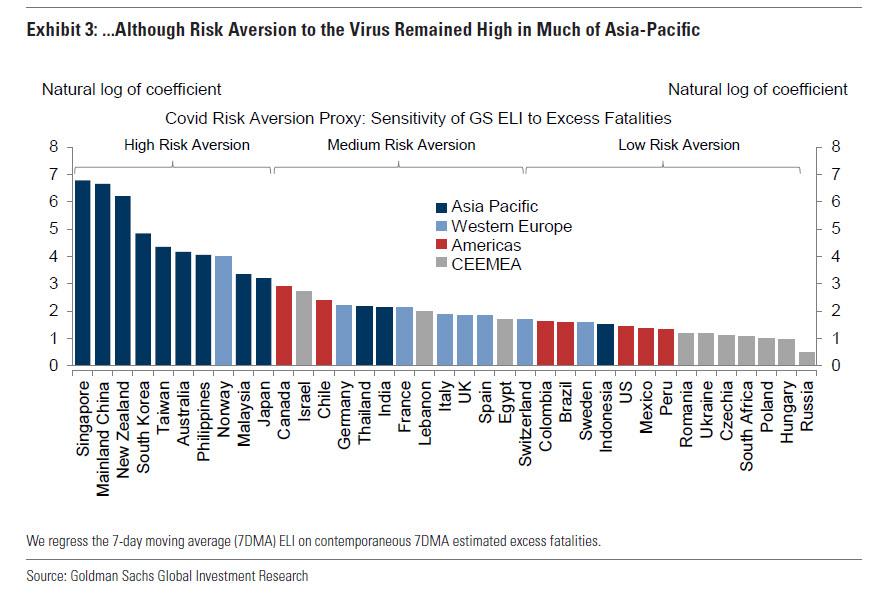

That said, risk aversion to covid remained high in much of Asia-Pacific where containment proved to be far more difficult.

Looking at the policy response, Goldman notes that fiscal policy began to drag in the US where Biden's Build Back Better crashed and burned in Congress, but remained expansionary in the Euro Area thanks to pent-up savings (which however, we contend have been largely spent by the lower and middle classes, an argument which Morgan Stanley has also made repeatedly).

Goldman's own output gap estimates tightened into overheating territory in the UK, and to a lesser extent in the Euro area and the US...

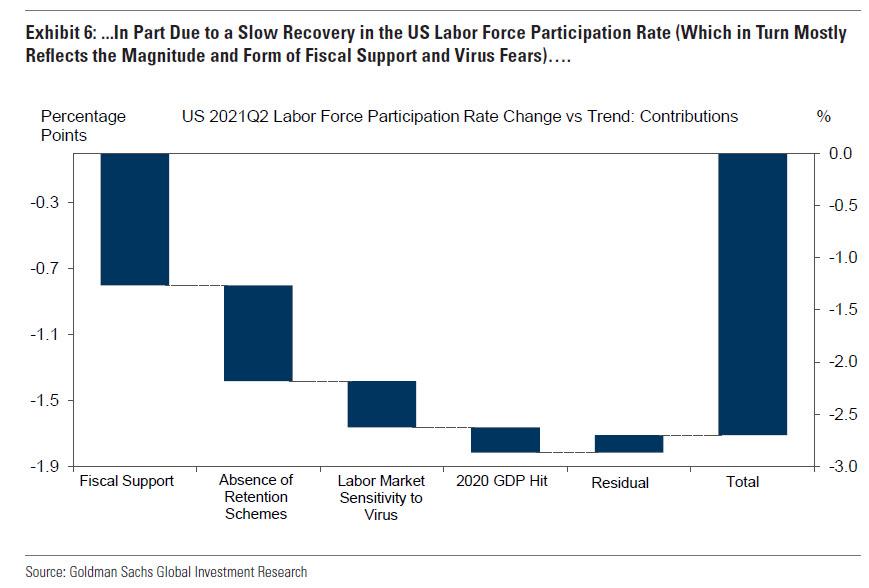

... which according to Goldman was due in part to a slow recovery in the labor force participation rate as workers simply refused to get back to the labor force.

And with fewer available workers, wage growth surged in the US and UK, and to a lesser extent in the Euro area.

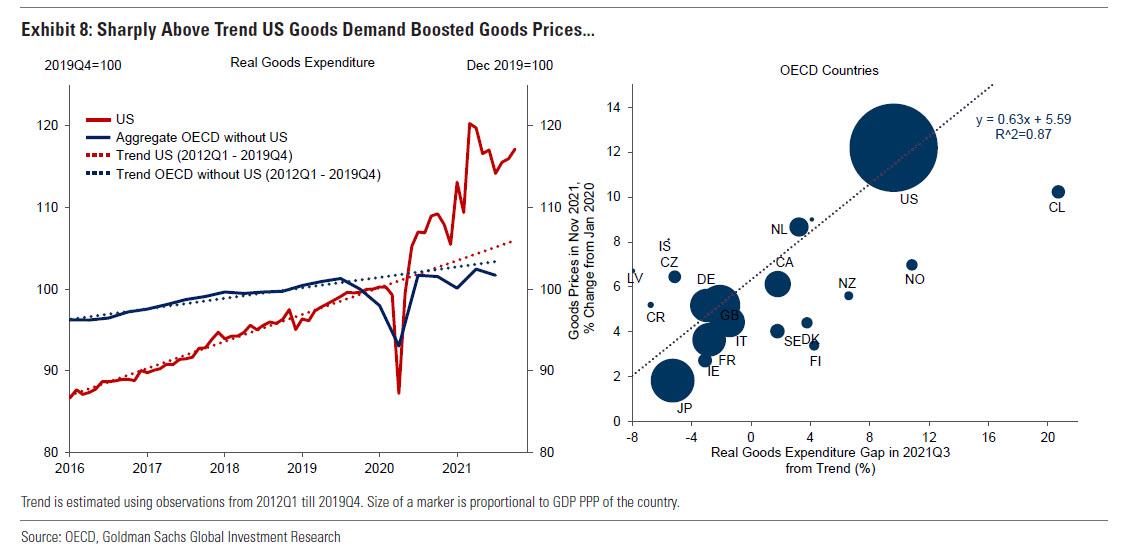

Meanwhile, the sharply above trend demand for US goods boosted goods prices...

... while together with impaired supply led to much higher than expected inflation in most G10 economies.

Finally, in response to soaring prices, G10 central banks "tapered or ended" QE much sooner than expected, and with the Fed preparing for rates liftoff as soon as mid-2022, the normalization process already started in Norway, New Zealand, UK and much of LatAm and CEEMEA.

Source : https://www.zerohedge.com/markets/goldmans-top-charts-2021