Author: Elite Forex Blog - Market Research & Analysis

EES: Tradestation a great option for US Forex traders

US based Forex traders still have a great option to trade Forex with automated systems – Tradestation. Tradestation EasyLanguage is simple to code your automated system. Forex accounts funded with $2,000 have no platform fee!

TradeStation- Trade with the online broker ranked best by Barron’s – Open an account today!

EES: Russia and China to impact Forex market dynamics

In response to sanctions, Russia is seeking non-USD trade deals, most notably with China. How will non-USD transactions impact the Forex market? Already, US based intellectuals are calling for an end to the Dollar Hegemony:

Note that as long as the dollar is the reserve currency, America’s trade deficit can worsen even when we’re not directly in on the trade. Suppose South Korea runs a surplus with Brazil. By storing its surplus export revenues in Treasury bonds, South Korea nudges up the relative value of the dollar against our competitors’ currencies, and our trade deficit increases, even though the original transaction had nothing to do with the United States.This isn’t just a matter of one academic writing one article. Mr. Austin’s analysis builds off work by the economist Michael Pettis and, notably, by the former Federal Reserve chairman Ben S. Bernanke.

Russia and China are agreeing to settle more trade in Rubles and Yuan. From Reuters:

(Reuters) – Russia and China pledged on Tuesday to settle more bilateral trade in rouble and yuan and to enhance cooperation between banks, Russia’s First Deputy Prime Minister Igor Shuvalov said, as Moscow seeks to cushion the effects of Western economic sanctions. Shuvalov told reporters in Beijing that he had agreed an economic cooperation pact with China’s Vice Premier Zhang Gaoli that included boosting use of the rouble and yuan for trade transactions. The pact also lets Russian banks set up accounts with Chinese banks, and makes provisions for Russian companies to seek loans from Chinese firms. “We are not going to break old contracts, most of which were denominated in dollars,” Shuvalov said through an interpreter. “But, we’re going to encourage companies from the two countries to settle more in localcurrencies, to avoid using a currency from a third country.”

China has an explosive Forex market, and is negotiating swap arrangements with other central banks. Retail demand for Forex in China is also exploding. Although the US Forex market is not developed as in Europe, Asia, and the UK, the USD has been the global reserve currency since World War 2. How will new players such as Russia and China impact the Forex market, and values of other currencies? Certainly, they will not take the same view as the US.

The free-floating Forex system we have today was in fact created by the US (Nixon Shock) but since no standards were ever established, now it’s an unknown unknown how the BRICs will evolve the Forex market, but certainly it will be changed forever. And certainly we can expect extreme volatility in the years ahead, even on the majors.

Continue Reading

Interbank FX transfers MT4 accounts to FXCM

Dear valued client,

As you may already have heard, TradeStation has announced an agreement between its IBFX, Inc. and IBFX Australia Pty Ltd subsidiaries, and a subsidiary of FXCM Inc., in which all retail accounts in the “MetaTrader/MT4” division of both IBFX forex subsidiaries will be transferred to FXCM.

Having supported two forex business lines – MT4 and TradeStation – for some time, we have now decided to focus solely on our TradeStation Forex platform offering.

TradeStation’s success over the past 15 years is due in large part to the unique, differentiating features and functions offered by the TradeStation platform, and this move will enable us to focus our resources on continuing that success.

This change will not affect your TradeStation Forex account(s). Should you have any questions, please contact us.

Sincerely yours,

Gary Weiss,

President of IBFX, Inc.

De-Dollarization Continues: China-Argentina Agree Currency Swap, Will Trade In Yuan

It appears there is another nation on planet Earth that is becoming isolated. One by one, Russia and China appear to be finding allies willing to ‘de-dollarize’; and the latest to join this trend is serial-defaulter Argentina. As Reuters reports, China and Argentina’s central banks have agreed a multi-billion dollar currency swap operation “to bolster Argentina’s foreign reserves” or “pay for Chinese imports with Yuan,” as Argentina’s USD reserves dwindle. In addition, Argentina claims China supports the nation’s plans in the defaulted bondholder dispute.

Having met ‘on the sidelines’ in Basel, Switzerland in July, Argentine and Chinese central banks agreed to a currency swap equivalent to $11b that Cabinet Chief Jorge Capitanich said could be used to stabilize reserves.. (as Reuters reports)

Argentina, which defaulted on its debt in July, will receive the first tranche of a multi-billion dollar currency swap operation with China’s central bank before the end of this year, the South American country’s La Nacion newspaper reported on Sunday.The swap will allow Argentina to bolster its foreign reserves or pay for Chinese imports with the yuan currency at a time weak export revenues and an ailing currency have put the Latin American nation’s foreign reserves under intense pressure.La Nacion said Argentina would receive yuan worth $1 billion by the end of 2014, the first payment of a loan worth a total $11 billion signed by Argentina’s President Cristina Fernandez and her Chinese counterpart in July.

In adition, Bloomberg reports

Continue ReadingPeople’s Bank of China Governor Zhou Xiaochuan expressed his support for Argentina in its legal fight against holdout bondholders

EES: Snap up .cash and .fund for your investment business

FX System Hosting now offering .cash .tax and .fund top level domains for your investment related website.Get a .cash for your Forex company, Forex managed accounts program or signal service, or other financial business. Order one at www.fxsyste…

Continue Reading

In Shocking Move, ECB Cuts By 10 Bps, Sends Deposit Rate Further Into Negative Territory

While everyone was expecting Mario Draghi to announce ABS purchases, few if any had expected the ECB to also cut rates. Which it just did whacking its corridor rates across the board by 10 bps, in the process sending the Deposit Facility rate even further into negative territory, now down at -0.2%.

From the ECB’s monetary policy decision:

At today’s meeting the Governing Council of the ECB took the following monetary policy decisions:

- The interest rate on the main refinancing operations of the Eurosystem will be decreased by 10 basis points to 0.05%, starting from the operation to be settled on 10 September 2014.

- The interest rate on the marginal lending facility will be decreased by 10 basis points to 0.30%, with effect from 10 September 2014.

- The interest rate on the deposit facility will be decreased by 10 basis points to -0.20%, with effect from 10 September 2014.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 2.30 p.m. CET today.

To be sure, the EURUSD is down nearly 100 pips on the news, and this is even before Draghi has announced his “Private QE” which announcement is due in 45 minutes.

So now that it will cost Europeans even more to deposit money at the bank, here is a snapshot of how delighted, giddy locals from the Old Continent are reacting to this latest ploy to fix “stuff” by the ECB.

http://www.zerohedge.com/news/2014-09-04/shocking-move-ecb-cuts-10-bps-sends-deposit-rate-further-negative-territory

Trade the Euro – Open a Forex Account

Continue Reading Trade the Euro – Open a Forex Account

The Ultimate Demise Of The Euro Union

The European Union (EU) was created by the Maastricht Treaty on November 1st 1993. It is a political and economic union between European countries which makes its own policies concerning the members’ economies, societies, laws and to some extent security. To some, the EU is an overblown bureaucracy which drains money…and compromises the power of sovereign states. For others, the EU is the best way to meet challenges smaller nations might struggle with – such as economic growth or negotiations with larger nations – and worth surrendering some sovereignty to achieve. Despite many years of integration, opposition remains strong.

ACCORDINGLY, there are signs the EU is teetering on implosion.

Indeed the Euro zone break up is inevitable for numerous reasons.

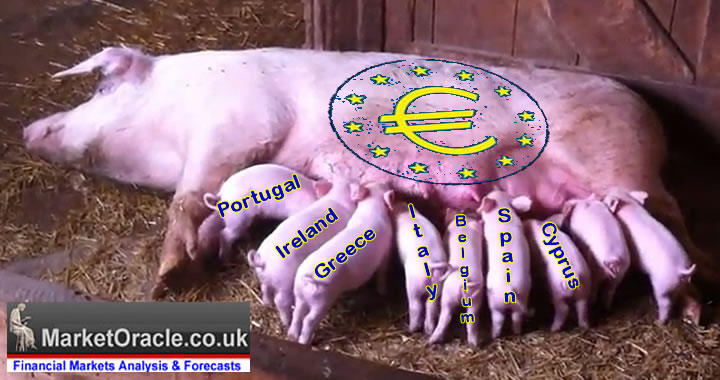

Unpayable government debts and the massive bailouts in Greece, Portugal, Spain and Ireland logically pave the road to an eventual EU break up.

While it’s convenient to have the one currency for 17 different nations, the nature of those national economies and their strength is quite different and problematic. Indeed and fact it favors wealthy countries like Germany and France at the expense of the PIIGS (i.e. Portugal, Italy, Ireland, Greece and Spain).

Another issue is that while the 17 nations share the same Central Bank, they do not have a central control on government budgets, nor central political control.

Paul Griffiths, Colonial First State chief investment officer does not want to put a time frame on the euro zone being shrunk, but says it will eventually be very different from what it is today.

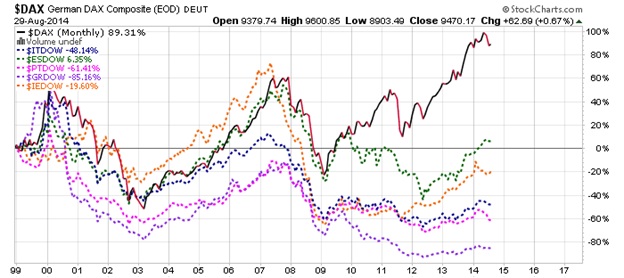

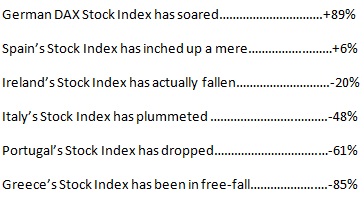

Unacceptable inequities of the EU are reflected in the Stock Market action of Germany vis-à-vis economically inferior members of the EU, commonly referred to as the PIIGS (i.e. Portugal, Italy, Ireland, Greece and Spain). Unabashedly Germany is living high on the hog (so to speak)…which translates to Germany living high on backs the PIIGS. To appreciate the gross disparity, compare the relative stock performances of their national Stock Indices.

PIIGS Stock Performance vs German DAX Index Since 1999

Literally, the PIIGS have been led to financial slaughter…while Germany lives high on the hog (pardon the pun).

——————————-

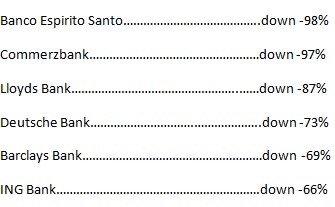

Cracks in the Banking Wall of the Euro Union

In recent years the financial backbone of Europe has been its banking sector. To be sure, a few old name (once) prestigious banks have suffered irresistible dumping of their stock by shareholders. Most devastated are Portuguese Banco Espirito Santo, German Commerzbank, Deutsche Bank and the National Bank of Greece.

Portuguese Banco Espirito Santo stock has plummeted -98 % from its 2007 high of $6.18…and sells today for a mere 12 cents a share. However, several other EU banks have suffered the same fate of relentlessly tumbling stock prices. The chart below shows the heart wrenching losses of share value since mid-2007, which include Commerzbank (Germany), Deutsche Bank (Germany), Barclays Bank UK), ING (Netherlands) and Lloyds (UK).

Negative stock performance for leading European Banks since mid-2007:

And then there is the National Bank of Greece, whose stock has plummeted -99.4% during the past seven years (See chart):

The only salvation for investors in the EU is GOLD

When the ultimate and inevitable demise of the EU begins to materialize, many wealthy Europeans from all member countries will flee to the traditional safe haven of gold. And although the UK is not a member of the EU, its FTSE Stock Index will understandably feel the adverse effects of pervasive stock dumping …ergo the FTSE will also suffer a sharp correction. Moreover, even the affluent Germans will stampede to buy gold…as they realize that gold has soared in value by +345% vs only +89% for the German DAX Stock Index during the past 15 years.

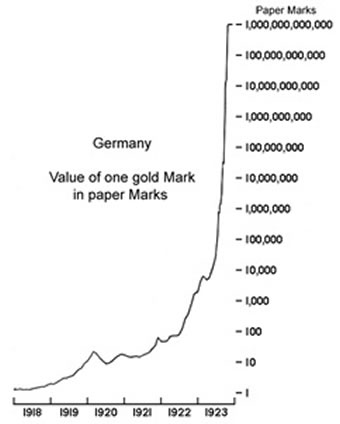

Germans Must Remember the Currency Tragedy of the Weimar Republic from 1918-1924

Students of German history will certainly remember what happened during the Hyper-Inflation of the Weimar Republic from 1918-1924, when German paper Marks became virtually worthLESS (See above chart):

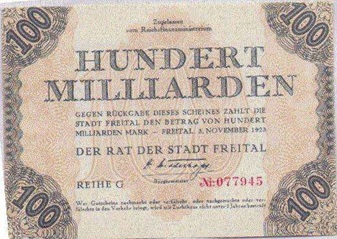

Moreover, the following will give the reader an idea of the viral currency inflation (monetary debasement) that plagued Germany from 1918-1924). Here is a photo of a German bank note for 100 Million Mark.

This near worthLESS bill represents 100 million. In fact in November 1923 One Billion would only buy 3 pounds of meat, or; 2 glasses of beer, or; one loaf of bread.

Although no one expects a repeat of the nightmarish 1918-1924 Hyper-Inflation, indubitably, the impending bust-up of the Euro Union will surely trash the paper Euro currency…as the heretofore members of the EU rush to re-establish their respective currencies. And as America’s greatest author Mark Twain once observed: “History doesn’t repeatitself, but it does rhyme.”

Related Study: “The Nightmare German Inflation”

And history is testament that the most devastating result of the Nightmarish Weimar Hyper-Inflation was an open door for Adolph Hitler to publish his infamous book in 1925: Mein Kampf…which ultimately led him to dictatorial power in Germany. And the rest is the nightmarishly dark history leading to World War II, which was the deadliest military conflict in history…when over 60 million people were killed.

————————–

Related Analysis:

It is painfully obvious the EU is a political concoction designed to further a covert political agenda. Indeed and fact there is no legitimate or logical basis for its existence. Consequently, it will not…and cannot last.

Based upon the above analysis, the Ultimate Demise Of The Euro Union is inevitable. The only unknown is WHEN AND HOW. Will it be Germany throwing in the towel after years of supporting the PIIGS…or will it be the PIIGS desperately wising to be masters of their own economic fate and sovereignty by abandoning the Euro currency in order to re-establish their old currencies (albeit at substantially lower valuations with a view to stimulate and revitalize their export markets)?

Founder of GOLD-EAGLE in January 1997. Vronsky has over 40 years’ experience in the international investment world, having cut his financial teeth in Wall Street as a Financial Analyst with White Weld. He believes gold and silver will soon be recognized as legal tender in all 50 US states (Utah and Arizona having already passed laws to that effect). Vronsky speaks three languages with indifference: English, Spanish and Brazilian Portuguese. His education includes university degrees in Engineering, Liberal Arts and an MBA in International Business Administration – qualifying as Phi Beta Kappa for high scholastic achievement in all three.

Continue Reading

The Nail In The Petrodollar Coffin: Gazprom Begins Accepting Payment For Oil In Ruble, Yuan

Several months ago, when Russia announced the much anticipated “Holy Grail” energy deal with China, some were disappointed that despite this symbolic agreement meant to break the petrodollar’s stranglehold on the rest of the world, neither Russia nor China announced payment terms to be in anything but dollars. In doing so they admitted that while both nations are eager to move away from a US Dollar reserve currency, neither is yet able to provide an alternative.

This changed in late June when first Gazprom’s CFO announced the gas giant was ready to settle China contracts in Yuan or Rubles, and at the same time the People’s Bank of China announced that its Assistant Governor Jin Qi and Russian central bank Deputy Chairman Dmitry Skobelkin held a meeting in which they discussed cooperating on project and trade financing using local currencies. The meeting discussed cooperation in bank card, insurance and financial supervision sectors.

And yet, while both sides declared their operational readiness and eagerness to bypass the dollar entirely, such plans remained purely in the arena of monetary foreplay and the long awaited first shot across the Petrodollar bow was absent.

Until now.

According to Russia’s RIA Novosti, citing business daily Kommersant, Gazprom Neft has agreed to export 80,000 tons of oil from Novoportovskoye field in the Arctic; it will accept payment in rubles, and will also deliver oil via the Eastern Siberia-Pacific Ocean pipeline (ESPO), accepting payment in Chinese yuan for the transfers. Meaning Russia will export energy to either Europe or China, and receive payment in either Rubles or Yuan, in effect making the two currencies equivalent as far as the Eurasian axis is conerned, but most importantly, transact completely away from the US dollar thus, finally putin'(sic) in action the move for a Petrodollar-free world.

More on this long awaited first nail in the petrodollar coffin from RIA:

The Russian government and several of the country’s largest exporters have widely discussed the possibility of accepting payments in rubles for oil exports. Last week, Russia began to ship oil from the Novoportovskoye field to Europe by sea. Two oil tankers are expected to arrive in Europe in September.According to Kommersant, the payment for these shipments will be received in rubles.Gazprom Neft will not only accept payments in rubles; subsequent transfers via the ESPO may be paid for in yuan, the newspaper reported.According to the newspaper, the change in currency was made because of the Western sanctions against Russia.As a protective measure, Russia decided to avoid making its payments in US dollars, which can be tracked and controlled by the United States government, Kommersant reported.

“Protective measure” meaning that it was the US which managed to Plaxico itself by pushing Russia to transact away from the US Dollar, in the process showing the world it can be done, and slamming the first nail in the petrodollar’s coffin.

This is not surprising to anyone who has been following our forecast of the next steps in the transition from the Petrodollar to the Gas-O-Yuan. Recall from April:

The New New Normal flow of funds:

- Gazprom delivering gas to China.

- China Gazprom paying in Yuan (convertible into Rubles)

- Gazprom funding itself increasingly in Yuan.

- Russia buying Chinese goods and services in Yuan (convertible into Rubles)

And all of this with the US banker cartel completely disintermediated courtesy of the glaring absence of the USD in any of the above listed steps, or as some may call it: from the Petrodollar to the Gas-o-yuan (something 40 central banks have already figured out… just not the Fed).

Still confused? Then read “90% Of Gazprom Clients Have “De-Dollarized”, Will Transact In Euro & Renminbi” for just how Gazprom set the stage for the day it finally would push the button to skip the dollar entirely. Which it just did.

In conclusion we will merely say what we have said previously, and it touches on what will be the most remarkable aspect of Obama’s legacy, because while the hypocrite “progressive” president who even his own people have accused of being a “brown-faced Clinton” after selling out to Wall Street and totally wrecking US foreign policy abroad, is already the worst president in a century of US history according to public polls, the fitting epitaph will come when the president’s policies put an end to dollar hegemony and end the reserve currency status of the dollar once and for all, thereby starting the rapid, and uncontrolled, collapse of the US empire. To wit:

In retrospect it will be very fitting that the crowning legacy of Obama’s disastrous reign, both domestically and certainly internationally, will be to force the world’s key ascendent superpowers (we certainly don’t envision broke, insolvent Europe among them) to drop the Petrodollar and end the reserve status of the US currency.

As of this moment, both Russia and China have shown not on that it can be done, but it isdone. Expect everyone to jump onboard the new superpower axis bandwagon soon enough.

It Begins: Council On Foreign Relations Proposes That “Central Banks Should Hand Consumers Cash Directly”

… A broad-based tax cut, for example, accommodated by a program of open-market purchases to alleviate any tendency for interest rates to increase, would almost certainly be an effective stimulant to consumption and hence to prices. Even if households decided not to increase consumption but instead re-balanced their portfolios by using their extra cash to acquire real and financial assets, the resulting increase in asset values would lower the cost of capital and improve the balance sheet positions of potential borrowers. A money-financed tax cut is essentially equivalent to Milton Friedman’s famous “helicopter drop” of money

– Ben Bernanke, Deflation: Making Sure “It” Doesn’t Happen Here, November 21, 2002

A year ago, when it became abundantly clear that all of the Fed’s attempts to boost the economy have failed, leading instead to a record divergence between the “1%” who were benefiting from the Fed’s aritficial inflation of financial assets, and everyone else (a topic that would become one of the most discussed issues of 2014) and with no help coming from a hopelessly broken Congress (who can forget the infamous plea by a desperate Wall Street lobby-funding recipient “Get to work Mr. Chariman”), we wrote that “Bernanke’s Helicopter Is Warming Up.”

A year ago, when it became abundantly clear that all of the Fed’s attempts to boost the economy have failed, leading instead to a record divergence between the “1%” who were benefiting from the Fed’s aritficial inflation of financial assets, and everyone else (a topic that would become one of the most discussed issues of 2014) and with no help coming from a hopelessly broken Congress (who can forget the infamous plea by a desperate Wall Street lobby-funding recipient “Get to work Mr. Chariman”), we wrote that “Bernanke’s Helicopter Is Warming Up.”The reasoning was very simple: in a country (and world) drowning with debt, there are only two options to extinguish said debt: inflate it away or default. Anything else is kicking the can while making the problem even worse. Because while the Fed has been successful at recreating the world’s biggest asset bubble (in history), it has failed to stimulate broad, “benign” demand-pull inflation as the trickle down effects of its “wealth effect” have failed to materialize 6 years after the launch of the Fed’s unconventional monetary policies.

In other words, a world stuck in the last phase before complete Keynesian collapse, had no choice but to gamble “all in” with the last and only bluff it had left before admitting the economic system it had labored under, one which has borrowed so extensively from the future to fund the present that there is no future left, has failed.

The only question left was when would the trial balloons for such monetary paradrops start to emerge.

We now know the answer, and it is today.

Moments ago a stunning article appearing in the “Foreign Affaird” publication of the influential and policy-setting Council of Foreign Relations, titled “Print Less but Transfer More: Why Central Banks Should Give Money Directly to the People.”

In it we read the now conventional admission of failure by Keynesians, who however, unwilling to actually admit they have been wrong, urge the even more conventional solution: do more of the same that has lead to the current financial cataclysm, only in this case the authors advocate no longer pretending that the traditional monetary channels work but to, literally, paradrop money. To wit:

To some extent, low inflation reflects intense competition in an increasingly globalized economy. But it also occurs when people and businesses are too hesitant to spend their money, which keeps unemployment high and wage growth low. In the eurozone, inflation has recently dropped perilously close to zero. And some countries, such as Portugal and Spain, may already be experiencing deflation. At best, the current policies are not working; at worst, they will lead to further instability and prolonged stagnation.Governments must do better. Rather than trying to spur private-sector spending through asset purchases or interest-rate changes,central banks, such as the Fed, should hand consumers cash directly. In practice, this policy could take the form of giving central banks the ability to hand their countries’ tax-paying households a certain amount of money. The government could distribute cash equally to all households or, even better, aim for the bottom 80 percent of households in terms of income. Targeting those who earn the least would have two primary benefits. For one thing, lower-income households are more prone to consume, so they would provide a greater boost to spending. For another, the policy would offset rising income inequality.

A third, and most important outcome, would be the one we have forecast from the beginning of this ridiculous central bank experiment: “hyperinflation” (which is not simply runaway inflation as it is often incorrectly designated – it is outright evisceration of the prevailing monetary system), which has been avoided for now, but which is inevitable in a world in which only the wholesale destruction of the fiat reserve currency is the one option left to inflate away the debt overhang.

So without further ado, here is the first official trial balloon – the article that one day soon will be seen as the canary in the paradropmine, and the piece that will finally get the rotor of Bernanke’s, now Yellen’s infamous helicopter finally spinning. Highlights ours:

Print Less but Transfer More: Why Central Banks Should Give Money Directly to the People

From Foreign Affairs, by Mark Blyth and Eric Lonergan

In the decades following World War II, Japan’s economy grew so quickly and for so long that experts came to describe it as nothing short of miraculous. During the country’s last big boom, between 1986 and 1991, its economy expanded by nearly $1 trillion. But then, in a story with clear parallels for today, Japan’s asset bubble burst, and its markets went into a deep dive. Government debt ballooned, and annual growth slowed to less than one percent. By 1998, the economy was shrinking.

That December, a Princeton economics professor named Ben Bernanke argued that central bankers could still turn the country around. Japan was essentially suffering from a deficiency of demand: interest rates were already low, but consumers were not buying, firms were not borrowing, and investors were not betting. It was a self-fulfilling prophesy: pessimism about the economy was preventing a recovery. Bernanke argued that the Bank of Japan needed to act more aggressively and suggested it consider an unconventional approach: give Japanese households cash directly. Consumers could use the new windfalls to spend their way out of the recession, driving up demand and raising prices.

As Bernanke made clear, the concept was not new: in the 1930s, the British economist John Maynard Keynes proposed burying bottles of bank notes in old coal mines; once unearthed (like gold), the cash would create new wealth and spur spending. The conservative economist Milton Friedman also saw the appeal of direct money transfers, which he likened to dropping cash out of a helicopter. Japan never tried using them, however, and the country’s economy has never fully recovered. Between 1993 and 2003, Japan’s annual growth rates averaged less than one percent.

Today, most economists agree that like Japan in the late 1990s, the global economy is suffering from insufficient spending, a problem that stems from a larger failure of governance. Central banks, including the U.S. Federal Reserve, have taken aggressive action, consistently lowering interest rates such that today they hover near zero. They have also pumped trillions of dollars’ worth of new money into the financial system. Yet such policies have only fed a damaging cycle of booms and busts, warping incentives and distorting asset prices, and now economic growth is stagnating while inequality gets worse. It’s well past time, then, for U.S. policymakers — as well as their counterparts in other developed countries — to consider a version of Friedman’s helicopter drops. In the short term, such cash transfers could jump-start the economy. Over the long term, they could reduce dependence on the banking system for growth and reverse the trend of rising inequality. The transfers wouldn’t cause damaging inflation, and few doubt that they would work. The only real question is why no government has tried them.

EASY MONEY

In theory, governments can boost spending in two ways: through fiscal policies (such as lowering taxes or increasing government spending) or through monetary policies (such as reducing interest rates or increasing the money supply). But over the past few decades, policymakers in many countries have come to rely almost exclusively on the latter. The shift has occurred for a number of reasons. Particularly in the United States, partisan divides over fiscal policy have grown too wide to bridge, as the left and the right have waged bitter fights over whether to increase government spending or cut tax rates. More generally, tax rebates and stimulus packages tend to face greater political hurdles than monetary policy shifts. Presidents and prime ministers need approval from their legislatures to pass a budget; that takes time, and the resulting tax breaks and government investments often benefit powerful constituencies rather than the economy as a whole. Many central banks, by contrast, are politically independent and can cut interest rates with a single conference call. Moreover, there is simply no real consensus about how to use taxes or spending to efficiently stimulate the economy.

Steady growth from the late 1980s to the early years of this century seemed to vindicate this emphasis on monetary policy. The approach presented major drawbacks, however. Unlike fiscal policy, which directly affects spending, monetary policy operates in an indirect fashion. Low interest rates reduce the cost of borrowing and drive up the prices of stocks, bonds, and homes. But stimulating the economy in this way is expensive and inefficient, and can create dangerous bubbles — in real estate, for example — and encourage companies and households to take on dangerous levels of debt.

That is precisely what happened during Alan Greenspan’s tenure as Fed chair, from 1997 to 2006: Washington relied too heavily on monetary policy to increase spending. Commentators often blame Greenspan for sowing the seeds of the 2008 financial crisis by keeping interest rates too low during the early years of this century. But Greenspan’s approach was merely a reaction to Congress’ unwillingness to use its fiscal tools. Moreover, Greenspan was completely honest about what he was doing. In testimony to Congress in 2002, he explained how Fed policy was affecting ordinary Americans:

“Particularly important in buoying spending [are] the very low levels of mortgage interest rates, which [encourage] households to purchase homes, refinance debt and lower debt service burdens, and extract equity from homes to finance expenditures. Fixed mortgage rates remain at historically low levels and thus should continue to fuel reasonably strong housing demand and, through equity extraction, to support consumer spending as well.”

Of course, Greenspan’s model crashed and burned spectacularly when the housing market imploded in 2008. Yet nothing has really changed since then. The United States merely patched its financial sector back together and resumed the same policies that created 30 years of financial bubbles. Consider what Bernanke, who came out of the academy to serve as Greenspan’s successor, did with his policy of “quantitative easing,” through which the Fed increased the money supply by purchasing billions of dollars’ worth of mortgage-backed securities and government bonds. Bernanke aimed to boost stock and bond prices in the same way that Greenspan had lifted home values. Their ends were ultimately the same: to increase consumer spending.

The overall effects of Bernanke’s policies have also been similar to those of Greenspan’s. Higher asset prices have encouraged a modest recovery in spending, but at great risk to the financial system and at a huge cost to taxpayers. Yet other governments have still followed Bernanke’s lead. Japan’s central bank, for example, has tried to use its own policy of quantitative easing to lift its stock market. So far, however, Tokyo’s efforts have failed to counteract the country’s chronic underconsumption. In the eurozone, the European Central Bank has attempted to increase incentives for spending by making its interest rates negative, charging commercial banks 0.1 percent to deposit cash. But there is little evidence that this policy has increased spending.

China is already struggling to cope with the consequences of similar policies, which it adopted in the wake of the 2008 financial crisis. To keep the country’s economy afloat, Beijing aggressively cut interest rates and gave banks the green light to hand out an unprecedented number of loans. The results were a dramatic rise in asset prices and substantial new borrowing by individuals and financial firms, which led to dangerous instability. Chinese policymakers are now trying to sustain overall spending while reducing debt and making prices more stable. Like other governments, Beijing seems short on ideas about just how to do this. It doesn’t want to keep loosening monetary policy. But it hasn’t yet found a different way forward.

The broader global economy, meanwhile, may have already entered a bond bubble and could soon witness a stock bubble. Housing markets around the world, from Tel Aviv to Toronto, have overheated. Many in the private sector don’t want to take out any more loans; they believe their debt levels are already too high. That’s especially bad news for central bankers: when households and businesses refuse to rapidly increase their borrowing, monetary policy can’t do much to increase their spending. Over the past 15 years, the world’s major central banks have expanded their balance sheets by around $6 trillion, primarily through quantitative easing and other so-called liquidity operations. Yet in much of the developed world, inflation has barely budged.

To some extent, low inflation reflects intense competition in an increasingly globalized economy. But it also occurs when people and businesses are too hesitant to spend their money, which keeps unemployment high and wage growth low. In the eurozone, inflation has recently dropped perilously close to zero. And some countries, such as Portugal and Spain, may already be experiencing deflation. At best, the current policies are not working; at worst, they will lead to further instability and prolonged stagnation.

MAKE IT RAIN

Governments must do better. Rather than trying to spur private-sector spending through asset purchases or interest-rate changes, central banks, such as the Fed, should hand consumers cash directly. In practice, this policy could take the form of giving central banks the ability to hand their countries’ tax-paying households a certain amount of money. The government could distribute cash equally to all households or, even better, aim for the bottom 80 percent of households in terms of income. Targeting those who earn the least would have two primary benefits. For one thing, lower-income households are more prone to consume, so they would provide a greater boost to spending. For another, the policy would offset rising income inequality.

Such an approach would represent the first significant innovation in monetary policy since the inception of central banking, yet it would not be a radical departure from the status quo. Most citizens already trust their central banks to manipulate interest rates. And rate changes are just as redistributive as cash transfers. When interest rates go down, for example, those borrowing at adjustable rates end up benefiting, whereas those who save — and thus depend more on interest income — lose out.

Most economists agree that cash transfers from a central bank would stimulate demand. But policymakers nonetheless continue to resist the notion. In a 2012 speech, Mervyn King, then governor of the Bank of England, argued that transfers technically counted as fiscal policy, which falls outside the purview of central bankers, a view that his Japanese counterpart, Haruhiko Kuroda, echoed this past March. Such arguments, however, are merely semantic. Distinctions between monetary and fiscal policies are a function of what governments ask their central banks to do. In other words, cash transfers would become a tool of monetary policy as soon as the banks began using them.

Other critics warn that such helicopter drops could cause inflation. The transfers, however, would be a flexible tool. Central bankers could ramp them up whenever they saw fit and raise interest rates to offset any inflationary effects, although they probably wouldn’t have to do the latter: in recent years, low inflation rates have proved remarkably resilient, even following round after round of quantitative easing. Three trends explain why. First, technological innovation has driven down consumer prices and globalization has kept wages from rising. Second, the recurring financial panics of the past few decades have encouraged many lower-income economies to increase savings — in the form of currency reserves — as a form of insurance. That means they have been spending far less than they could, starving their economies of investments in such areas as infrastructure and defense, which would provide employment and drive up prices. Finally, throughout the developed world, increased life expectancies have led some private citizens to focus on saving for the longer term (think Japan). As a result, middle-aged adults and the elderly have started spending less on goods and services. These structural roots of today’s low inflation will only strengthen in the coming years, as global competition intensifies, fears of financial crises persist, and populations in Europe and the United States continue to age. If anything, policymakers should be more worried about deflation, which is already troubling the eurozone.

There is no need, then, for central banks to abandon their traditional focus on keeping demand high and inflation on target. Cash transfers stand a better chance of achieving those goals than do interest-rate shifts and quantitative easing, and at a much lower cost. Because they are more efficient, helicopter drops would require the banks to print much less money. By depositing the funds directly into millions of individual accounts — spurring spending immediately — central bankers wouldn’t need to print quantities of money equivalent to 20 percent of GDP.

The transfers’ overall impact would depend on their so-called fiscal multiplier, which measures how much GDP would rise for every $100 transferred. In the United States, the tax rebates provided by the Economic Stimulus Act of 2008, which amounted to roughly one percent of GDP, can serve as a useful guide: they are estimated to have had a multiplier of around 1.3. That means that an infusion of cash equivalent to two percent of GDP would likely grow the economy by about 2.6 percent. Transfers on that scale — less than five percent of GDP — would probably suffice to generate economic growth.

LET THEM HAVE CASH

Using cash transfers, central banks could boost spending without assuming the risks of keeping interest rates low. But transfers would only marginally address growing income inequality, another major threat to economic growth over the long term. In the past three decades, the wages of the bottom 40 percent of earners in developed countries have stagnated, while the very top earners have seen their incomes soar. The Bank of England estimates that the richest five percent of British households now own 40 percent of the total wealth of the United Kingdom — a phenomenon now common across the developed world.

To reduce the gap between rich and poor, the French economist Thomas Piketty and others have proposed a global tax on wealth. But such a policy would be impractical. For one thing, the wealthy would probably use their political influence and financial resources to oppose the tax or avoid paying it. Around $29 trillion in offshore assets already lies beyond the reach of state treasuries, and the new tax would only add to that pile. In addition, the majority of the people who would likely have to pay — the top ten percent of earners — are not all that rich. Typically, the majority of households in the highest income tax brackets are upper-middle class, not superwealthy. Further burdening this group would be a hard sell politically and, as France’s recent budget problems demonstrate, would yield little financial benefit. Finally, taxes on capital would discourage private investment and innovation.

There is another way: instead of trying to drag down the top, governments could boost the bottom. Central banks could issue debt and use the proceeds to invest in a global equity index, a bundle of diverse investments with a value that rises and falls with the market, which they could hold in sovereign wealth funds. The Bank of England, the European Central Bank, and the Federal Reserve already own assets in excess of 20 percent of their countries’ GDPs, so there is no reason why they could not invest those assets in global equities on behalf of their citizens. After around 15 years, the funds could distribute their equity holdings to the lowest-earning 80 percent of taxpayers. The payments could be made to tax-exempt individual savings accounts, and governments could place simple constraints on how the capital could be used.

For example, beneficiaries could be required to retain the funds as savings or to use them to finance their education, pay off debts, start a business, or invest in a home. Such restrictions would encourage the recipients to think of the transfers as investments in the future rather than as lottery winnings. The goal, moreover, would be to increase wealth at the bottom end of the income distribution over the long run, which would do much to lower inequality.

Best of all, the system would be self-financing. Most governments can now issue debt at a real interest rate of close to zero. If they raised capital that way or liquidated the assets they currently possess, they could enjoy a five percent real rate of return — a conservative estimate, given historical returns and current valuations. Thanks to the effect of compound interest, the profits from these funds could amount to around a 100 percent capital gain after just 15 years. Say a government issued debt equivalent to 20 percent of GDP at a real interest rate of zero and then invested the capital in an index of global equities. After 15 years, it could repay the debt generated and also transfer the excess capital to households. This is not alchemy. It’s a policy that would make the so-called equity risk premium — the excess return that investors receive in exchange for putting their capital at risk — work for everyone.

MO’ MONEY, FEWER PROBLEMS

As things currently stand, the prevailing monetary policies have gone almost completely unchallenged, with the exception of proposals by Keynesian economists such as Lawrence Summers and Paul Krugman, who have called for government-financed spending on infrastructure and research. Such investments, the reasoning goes, would create jobs while making the United States more competitive. And now seems like the perfect time to raise the funds to pay for such work: governments can borrow for ten years at real interest rates of close to zero.

The problem with these proposals is that infrastructure spending takes too long to revive an ailing economy. In the United Kingdom, for example, policymakers have taken years to reach an agreement on building the high-speed rail project known as HS2 and an equally long time to settle on a plan to add a third runway at London’s Heathrow Airport. Such large, long-term investments are needed. But they shouldn’t be rushed. Just ask Berliners about the unnecessary new airport that the German government is building for over $5 billion, and which is now some five years behind schedule. Governments should thus continue to invest in infrastructure and research, but when facing insufficient demand, they should tackle the spending problem quickly and directly.

If cash transfers represent such a sure thing, then why has no one tried them? The answer, in part, comes down to an accident of history: central banks were not designed to manage spending. The first central banks, many of which were founded in the late nineteenth century, were designed to carry out a few basic functions: issue currency, provide liquidity to the government bond market, and mitigate banking panics. They mainly engaged in so-called open-market operations — essentially, the purchase and sale of government bonds — which provided banks with liquidity and determined the rate of interest in money markets. Quantitative easing, the latest variant of that bond-buying function, proved capable of stabilizing money markets in 2009, but at too high a cost considering what little growth it achieved.

A second factor explaining the persistence of the old way of doing business involves central banks’ balance sheets. Conventional accounting treats money — bank notes and reserves — as a liability. So if one of these banks were to issue cash transfers in excess of its assets, it could technically have a negative net worth. Yet it makes no sense to worry about the solvency of central banks: after all, they can always print more money.

The most powerful sources of resistance to cash transfers are political and ideological. In the United States, for example, the Fed is extremely resistant to legislative changes affecting monetary policy for fear of congressional actions that would limit its freedom of action in a future crisis (such as preventing it from bailing out foreign banks). Moreover, many American conservatives consider cash transfers to be socialist handouts. In Europe, which one might think would provide more fertile ground for such transfers, the German fear of inflation that led the European Central Bank to hike rates in 2011, in the middle of the greatest recession since the 1930s, suggests that ideological resistance can be found there, too.

Those who don’t like the idea of cash giveaways, however, should imagine that poor households received an unanticipated inheritance or tax rebate. An inheritance is a wealth transfer that has not been earned by the recipient, and its timing and amount lie outside the beneficiary’s control. Although the gift may come from a family member, in financial terms, it’s the same as a direct money transfer from the government. Poor people, of course, rarely have rich relatives and so rarely get inheritances — but under the plan being proposed here, they would, every time it looked as though their country was at risk of entering a recession.

Unless one subscribes to the view that recessions are either therapeutic or deserved, there is no reason governments should not try to end them if they can, and cash transfers are a uniquely effective way of doing so. For one thing, they would quickly increase spending, and central banks could implement them instantaneously, unlike infrastructure spending or changes to the tax code, which typically require legislation. And in contrast to interest-rate cuts, cash transfers would affect demand directly, without the side effects of distorting financial markets and asset prices. They would also would help address inequality — without skinning the rich.

Ideology aside, the main barriers to implementing this policy are surmountable. And the time is long past for this kind of innovation. Central banks are now trying to run twenty-first-century economies with a set of policy tools invented over a century ago. By relying too heavily on those tactics, they have ended up embracing policies with perverse consequences and poor payoffs. All it will take to change course is the courage, brains, and leadership to try something new.

Continue Reading